Description

SUMMARY

Douglas is a well-known, high-quality, defensive growth business that recently went public in Germany and can be purchased for 6x earnings. We believe the earnings and the multiple will be significantly higher in a couple of years.

BUSINESS

Douglas is the largest premium beauty specialty retailer in Continental Europe, selling fragrances (~55% of sales), color cosmetics (~20%), skin care (~20%), and hair care and accessories. It attributes 67% of its sales to stores and 33% to e-commerce. Douglas’ key segment sales are 47% DACHNL (Germany, Austria, Switzerland, Netherlands, Belgium), 19% France, and 15% each Southern Europe (Italy, Spain, Portugal, Croatia, Slovenia) and Central-Eastern Europe (Poland, Czech, Slovakia, Hungary, Romania, Bulgaria, Latvia, Lithuania, Estonia). It operates 1,903 stores primarily under the Douglas banner, as well as Nocibé in France.

- Is Netflix undervalued?

- Is Netflix a buy?

- Is Netflix a good investment

- Is Disney undervalued?

- Is Disney a buy?

- Is Disney a good investment

Douglas is the largest player in most countries it operates in, with the main exception of France where it is number two. Based on sales in Germany, the Netherlands, France, Italy, and Poland (81% of the Continental market), Douglas has 23% market share. Sephora has 12%, and Marionnaud (the other Continental omnichannel competitor) has 5%.

European premium beauty specialty retail is an attractive market. About half of purchases are for a type of product that is new to the consumer. While the other half of purchases are for replacement, almost half of those purchases involve switching product/brand or seeking inspiration and guidance. As such consumers like to visit stores to see, feel, sample and learn about products in person. This is particularly important since most products cannot be returned once they are opened. Physical stores play a role in over 80% of customer journeys. Top retailers then utilize loyalty programs and omnichannel distribution to capture their customers’ online purchases as well.

Retailers like Douglas are valuable partners to premium beauty brands. Consumers like to learn about and purchase products from multiple brands but prefer to do so from a limited number of retailers. Brands partner with Douglas to market their brands and products in stores and online in a cohesive fashion, including placing brand advisors in Douglas stores. Brands may also prefer to work with a smaller number of larger retailers as it reduces the risk of product leaking into the grey market.

In Continental Europe premium beauty retail is conducted 25% through chain specialty retail stores, 20% through e-commerce, and 15-20% through travel retail stores. The rest of the market is split roughly evenly among department stores, independent retail stores, and pharmacies and spas.

- Is Google undervalued?

- Is Google a buy?

- Is Google a good investment

- Is Walmart undervalued?

- Is Walmart a buy?

- Is Walmart a good investment

It is important to be aware of the key similarities and differences between Douglas and Sephora. (1) While Douglas is larger than Sephora in its market, Sephora’s worldwide sales are about 3.4x those of Douglas. As a result, Sephora may have better insight on emerging consumer trends than Douglas. Also, Sephora could get better pricing from global brands, though these brands are also aware of the need to maintain a competitive retail environment. (2) Sephora is owned by LVMH and favors LVMH brands. (3) Douglas Beauty Card is the world’s largest such loyalty program, with over 59M members as compared to 44M for Ulta and over 40M for Sephora. 74% of Douglas’ sales are from Beauty Card members. (4) Douglas stores have a calmer feel while Sephora stores are more vibrant. (5) The average Sephora store generates about one-third more sales than the average Douglas store.

BACKGROUND

Douglas originated in 1821 as a soap factory in Hamburg, Germany. In 1910 the first Douglas store opened under a name license. In 1969 Hussel (a public company led by the Kreke family) acquired the six Douglas stores that existed at the time and began expanding the business. In 1989 Hussel was renamed Douglas. In 2013 Douglas went private with Advent International and the Kreke family, and in 2015 CVC became the majority shareholder. Douglas held its IPO in March 2024 at a price of €26.

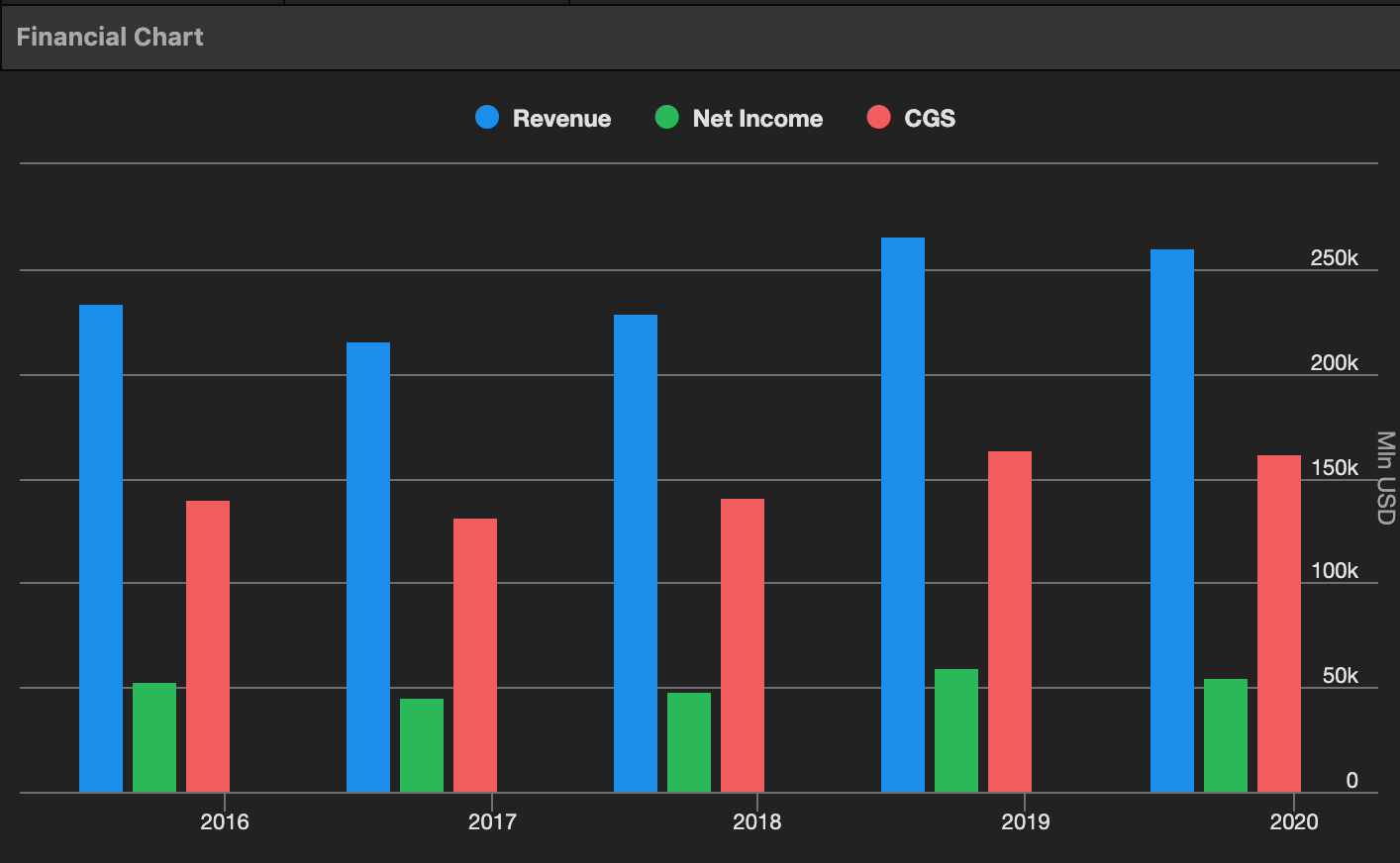

On December 19 Douglas announced its September quarter results and issued guidance for the fiscal year ended September 2025. At that time management said the new year had “started well” with “very strong” results to date including Black Friday. Douglas’s CFO and founding family both bought stock following the report. On an investor call at the beginning of January 2024, Douglas’ CFO said they had not seen any significant change in consumer behavior in calendar 2024 and that all markets were looking good, with Christmas showing a similar trend to the earlier part of the quarter. Then on February 13 Douglas announced its December quarter results. Revenue missed consensus by 1% and EBITDA missed by 4%, and management said FY EBITDA results would be at the lower end of guidance. Management said they saw a slowdown in the last two weeks of December and attributed it to (1) general negative consumer sentiment especially in Germany and France, (2) a slowdown in premium beauty in Europe, and (3) a very late Black Friday which ate into Christmas sales especially in Germany and France. Management also said the first weeks of January were also slow. Douglas’ stock fell 16% over the next two days.

WHY DOES THIS OPPORTUNITY EXIST?

- German IPO: These are not typically met with the same exuberance as those in the US.

- Financial leverage: Douglas is at 2.3x net debt/LTM EBITDA on a post-IFRS 16 basis.

- “One-time” add-backs: These amounted to 11% of FY 22 EBITDA, 6% of FY 23 EBITDA, and 10% of FY 24 EBITDA.

- Overhang: 69% of shares are held by CVC and the Kreke family (84-87% of that by CVC). As it has been nine years since CVC acquired its stake, it seems likely they will need to sell sooner rather than later. This overhang is exacerbated as the vast majority of the controlling shares secure a €300M margin loan. A July 2024 news article indicated a decline in the stock price to the €13-18 range would trigger a margin call.

- Bias: Professional investors tend to be men who are less interested in and may not implicitly understand the beauty industry.

- Uncertainly regarding recent results.

THESIS

- Douglas is a top player in an attractive business and will re-value as investors become familiar with it.

Premium beauty retail benefits from secular tailwinds. (i) Beauty generally seems to be gaining share of wallet over time, driven by social media. Social media promotes beauty products both by normalizing their consumption and driving product and brand discovery, likely leading to increased purchasing. (ii) The ongoing premiumization of beauty products drives share gains by the premium channel. (iii) Department stores and independent retailers are likely donating share to the premium retail channel over time. (iv) Men are slowly becoming a more important part of the customer base. There is a lot of potential when an industry that historically targeted only half the population starts serving the other half as well. (v) Social media makes it less expensive to launch new brands, fragmenting the supply base and driving value to the retail channel.

Premium beauty has also proven itself to be a defensive business. In the 2008-2010 period, Douglas’ inflation-adjusted LFL was down ~3% while EBITDA margin was down ~100bp. In 2011-2013 (another recession in Europe), inflation-adjusted LFL was up ~1% and EBITDA margin was flat.

Douglas is one of its premier participants in the industry and has particular growth opportunities. (i) It is in the middle of a three-year store refurbishment and expansion program. (ii) It is in the middle of a distribution center consolidation and upgrade program which is leading to greater product availability, quicker shipments, lower costs, and reduced working capital. (iii) It is in the midst of a technology infrastructure upgrade that, combined with the Douglas Beauty card, could lead to greater personalized marketing capabilities and improved predictive analytics. (iv) It intends to increase its sales of hair care products, which are a large part of the overall market.

Douglas also has very low working capital requirements for a retailer at ~1% of revenue by our calculation.

- The “one-time” costs are in the past. Douglas has guided to a “significant” reduction in these costs in FY 25 and for them to decline to under 1% of sales in the medium term. They were 0.4% of EBITDA in the last two quarters.

- Douglas will de-lever, start paying a dividend, and possibly repurchase shares. Douglas intends to begin paying 40% of its net income as dividends once leverage is around 2x and recently reiterated it will achieve that target after the December 2025 quarter. That likely means it will be a significant dividend payor in CY 26. Douglas could use the other 60% of its net income (which approximates free cash flow) to repurchase shares, perhaps from CVC.

- CVC will reduce its stake and the overhang will dissipate. CVC’s plan may anticipate a much higher stock in a couple years, after Douglas begins paying a dividend.

- There is little risk of forced selling via margin call. The controlling shareholders’ stake is valued at ~5x the size of the margin loan and CVC is a €25B market cap company with plentiful financial resources.

- Douglas could be acquired. Media reports indicate that before CVC acquired Douglas in 2015 there was also interest from LVMH, CVS (the US drugstore), an Asian bidder (possibly Hutchison Whampoa, owner of Marionnaud), and KKR. Ulta could be an interested party today, as merging with Douglas would provide Ulta with similar global heft to Sephora.

As to why CVC opted for an IPO rather than selling, it is possible CVC pursued an IPO because the Kreke family wanted to remain involved. The two groups have a shareholders’ agreement which requires them to agree on certain significant matters, probably including a sale. Notably Douglas’ Honorary Chairman Jörn Kreke passed away one month before Douglas went public this year. Dr. Kreke drove the acquisition of Douglas in 1969 and was CEO until 2001 and Chairman until his retirement in 2014. Rather than selling shares in the IPO, the controlling shareholders contributed another €300M of equity to de-lever the company.

Media reports indicate that before CVC acquired Douglas in 2015 there was also interest from LVMH, CVS (the US drugstore), an Asian bidder (possibly Hutchison Whampoa, owner of Marionnaud), and KKR. Ulta could be an interested party today, as merging with Douglas would provide Ulta with similar global heft to Sephora.

- Recent results may not be a harbinger of doom. Douglas’ segment results reveal the CQ4 issue to have been in the DACHNL region, which is primarily Germany. LFL went from 12.7% in CQ3 to 5.2% in CQ4, and EBITDA margin declined 90bp to 21.7%. German retail data through does not indicate anything amiss, including specifically for “cosmetic and toiletry articles”. Beauty suppliers who have reported CQ4 results have indicated Europe is fine. As recently as early January management said all is well. So how could they have reported a dramatic slowdown impacting only the last 13 days of the quarter? Frankly, answering this question is work-in-progress and there could be two co-existing answers.

First, it’s possible that this large omnichannel retailer does not have adequate data to monitor sales at a regional level in real time or management does know how to utilize such data. Douglas has been in the midst of multi-year project to update and harmonize its omnichannel IT platform. This project is well over half-completed, with the full stack having been rolled out in DACHNL over one year ago. That said, it’s possible consolidated sales have a lag to them and that management did not otherwise notice the DACHNL slowdown as of early January. (This should be easy to figure out.)

Second, it has been suggested that Flaconi (a German online beauty retailer) became very aggressive in the back half of December. Flaconi has been in a sale process since last April and may have taken such action in order to show strong revenue growth. If this is a problem it is likely to be a fleeting issue. (This is diligence in process.)

Finally, it is notable that Douglas CFO purchased €274K of stock on February 17.

Stepping back, we think it is unlikely a good business like this is suddenly falling apart, the reward to risk is highly favorable for investors who can take a longer view, and we are willing to buy into uncertainty while we complete our diligence.

EQUITY MARKET AND ECONOMIC BACKDROP

European stock valuations have risen this year. The Euro Stoxx Large index is at a forward P/E of 15.2x compared to 13.9x at the end of 2024 and a median of 12.6x in 2006-07 and 13.7x in 2014-19. European ten-year government bonds yield 2.5% vs a median 3.4% in 2006-07 and 0.4% in 2014-19.

The EU economy seems lukewarm. Real GDP has grown at a 0.8% CAGR and reail retail sales at a 2.1% CAGR since Q3 2023. Consumer confidence has generally improved to near its long-term average since hitting an all-time low Q3 22, but it did worsen a bit in November and December 2024.

- Is Apple undervalued?

- Is Apple a buy?

- Is Apple a good investment

- Is Nvidia undervalued?

- Is Nvidia a buy?

- Is Nvidia a good investment

FINANCIAL PROJECTIONS

We model Douglas’ revenue going forward based on based on LFL growth and store growth. We assume the store growth and remodel program is complete by the end of FY 26, and that LFLs drop to 3% in FY 29. We assume gross margins stabilize at FY 24 levels, while operating expenses provide modest incremental leverage.

Our base case reflects company guidance. Our bear case assumes inflation-adjusted LFL declines 3.0% in FY 26 before assuming the base case trajectory.

END OF FY 2026 PRICE TARGETS

In the base case we assume Douglas trades at 15x unlevered FCF. This implies 14.6x EPS with a 2.7% dividend yield. At that time Douglas would be levered at 1.7x post-IFRS 16 or 0.9x pre-IFRS 16. This leads to a price of €55 per share.

In the bear case we assume 10x unlevered FCF. This implies 8.8x EPS with a 4.5% dividend yield. At that time Douglas would be levered at 2.0x post-IFRS 16 or 1.2x pre-IFRS 16. This leads to a price of €29.

OTHER VALUE INDICATORS

Private market value: CVC acquired Douglas in 2015 for 8.8x 2016 EBITDA (pre-IFRS 16). Douglas currently trades at 4.4x EBITDA on a comparable basis.

Comps: There is not a great comp for Douglas, but these companies provide some potential indications of value.

- Ulta, the most similar public company, trades in the US with a $19B market cap at 17x EPS.

- Fielman, a vertically integrated optical retailer, trades in Germany with a €4B market cap at 19x EPS and a 3.2% dividend yield.

- Matas, Douglas’ Nordic doppelganger, trades in Denmark with a €700M market cap at 12x EPS and a 2.2% dividend yield.

Insider activity: The Kreke family purchased €13M of stock at an average price of €20 on 27 days between May 31 and September 13, 2024, and €3M of stock also at an average price of €20 between December 20 and December 30, 2024. Douglas’ CEO purchased €299K at an average price of €20 at the end of May 2024, and its CFO purchased €197K at €19.50 on December 20, 2024 and then €274K at €16.35 on February 17, 2024.