Heico Corporation

Introduction

Heico Corporation (Heico or HEI) is a global designer and manufacturer of highly engineered components for aviation, defense, and space markets. The company was founded in 1957 but current management assumed control of the company in 1990. The company is led by Chairman and CEO Laurans Mendelson and his sons, Co-Presidents, Eric and Victor Mendelson. Laurans Mendelson is 84 years old and Eric and Victor are 57 and 55 years old, respectively. Since the Mendelsons gained control of the company, the performance of the business as well as returns to shareholders has been nothing short of miraculous. Since 1990, the family has transformed Heico from a money-losing company worth $25 million with $26 million in sales to a company today worth $20.9 billion with sales and profits of $2.74 billion and $400 million, respectively.

The company’s value has compounded at 22% annually since 1990 due to several factors including a focus on designing and manufacturing aftermarket aerospace components, designing and manufacturing mission critical, highly specialized electronic components for niche markets in aerospace and defense and successfully executing a robust acquisition program. Management has overseen nearly 100 acquisitions since it took control and claims to have never had a failed deal, although some have worked out better than others. These acquisitions have led to significant revenue growth over time and, due to operating in attractive markets, organic growth has been strong as well. To its credit, management has been able to accomplish this impressive growth with only minimal increases in the share count over time. For example, diluted shares outstanding have only increased by less than 0.5% per year for the past 15 years. This is likely because the Mendelsons own significant amounts of Heico stock.

Heico has two share classes of stock: Common stock and Class A stock. The Common stock is entitled to 10 votes per share whereas the Class A is entitled to 1. Other than this voting difference, the shares are identical in all other aspects. Currently there are over 136.6 million shares outstanding which are comprised of 82.1 million A shares and 54.5 million Common shares. Given the voting differential, 87% of the voting power rests with the common shares, of which the Mendelsons own 17% and Heico management and employees (including the Mendelsons) own 20%. Including the A shares (which have the exact same economic rights) the Mendelsons collectively own 7.6% of the company, a stake which is worth $1.7 billion.

Segment Overview

Heico operates in two segments: the Flight Support Group (FSG) and the Electronic Technologies Group (ETG). In FY 2022, the company’s revenue totaled $2.21 billion, 56% of which of which came from FSG. 35% of sales are international. The company’s top five customers account for 21% of net sales. The FSG segment is the world’s largest manufacturer of non-original equipment manufacturer (OEM) aircraft component replacement parts and it also operates several FAA-approved maintenance, repair, and overhaul facilities (MRO) as well as provides distribution services for the aerospace market. It serves a wide range of customers including nearly all large commercial airlines and air cargo carriers, repair and overhaul facilities, OEMs, other aftermarket suppliers, and the US and foreign governments.

FSG competes with many leading aircraft component OEMs in the replacement part market as well as MRO service providers. Historically, the leading engine manufacturers as well as other OEM component manufacturers have been the sole provider for aircraft replacement parts. This is due primarily to an arduous FAA certification process which has created barriers to entry for component manufacturers. However, FSG has been very successful at overcoming these barriers and getting its replacement parts approved by the FAA which provides competition to the OEMs as well as significant savings to its customers. Every year on average, FSG receives FAA approval for 300 to 500 different replacement parts to add to its catalog of over 12,200 different parts. Over the past decade, Heico has doubled the number of replacement parts it offers, growing at an annual rate of 7.4%. Even though it is the leading global supplier of non-OEM aircraft replacement components, Heico still only has a MSD share of the total addressable component aftermarket, which leaves a long runway for growth.

FSG currently serves nearly all the world’s major airlines in some capacity, either through component sales, MRO services and/or parts distribution. In fact, FSG has partnership agreements with a number of large airlines including Lufthansa, British Air, Japan Airlines, American Airlines, Delta Airlines and United Airlines. Typically these agreements give Heico the exclusive right to manage the non-OEM parts programs for these airlines and also lead to close collaboration on future part development and MRO services. Lufthansa actually owns a minority interest in an FSG subsidiary based on an agreement made in 1997 in an effort to circumvent the OEM monopoly and better control costs for both components and MRO work.

The ETG segment designs and manufactures “highly-engineered, mission-critical subcomponents that must successfully operate in the harshest environments, for smaller, niche markets, but which are utilized in larger systems – systems like power, targeting, tracking, identification, simulation, testing, communications, lighting, surgical, medical imaging, baggage scanning, telecom and computer systems. These systems are, in turn, often located on another platform, such as aircraft, rotorcraft, satellites, ships, spacecrafts, land vehicles, handheld devices and other platforms.”[1] Over half of ETG’s revenues are tied to the defense industry, including sales to the US and foreign government as well as defense contractors. ETG is a leader in equipment used in the development of missile seeking technology and airborne and shipboard targeting and reconnaissance systems, including the Patriot Missile System and Predator Drone. It is also the industry leader in underwater locator beacons which are used to locate submerged aircraft cockpit voice recorders and flight data records. With the exception of medical devices, most ETG products are found on things that fly, primarily spacecraft, satellites, planes, and rotorcraft. For example, ETG supplied memory modules for the data recorder and power converters and electromagnetic interference filters for NASA’s New Horizons spacecraft which reached Pluto a few years ago after being launched in 2006. ETG also supplied memory modules for the Philae spacecraft which landed on a comet in 2015 after a ten-year journey.

The company had this to say about ETG in the 2009 annual report:

We view our Electronic Technologies companies as solution providers, not hardware providers. By taking this view, we become seamless with our customers’ design activities and we are partners in getting their programs delivered on time, within cost estimates and functioning perfectly like they intend. While our ultimate sale is typically a piece of physical product that is then integrated into a larger subsystem, we know that our unique and proprietary know-how separates us from mere “commodity” suppliers.

Parts Manufacturers Approval

- Apple Dividend

- Microsoft Dividend

- Exxon Dividend

- Wells Fargo Dividend

- Pfizer Dividend

- Coca-Cola Dividend

- Verizon Dividend

- Frontline Dividend

- Costco Dividend

- Home Depot Dividend

For all planes flying in the US (and by proxy, around the world), there is a rigorous FAA certification process. For a replacement part to be sold for use on an aircraft, it either has to be manufactured by the original equipment manufacturer (OEM) or it must receive separate approval from the FAA. While it is possible for a secondary supplier to get a replacement part FAA certified, this can be an expensive and time-consuming process.

As previously mentioned, Heico’s FSG division is the world’s largest manufacturer of FAA-approved jet engine and aircraft component replacement parts other than the OEMs. These replacement parts, which are new and have been approved by the FAA, are referred to as PMA (Parts Manufacturers Approval) parts. The PMA is a combined design and production approval granted by the FAA for replacement parts for aircraft which are not manufactured by the OEMs. PMA producers claim that often their components are of higher quality than the original OEM part because can have the benefit of observing how a part wears over time and can potentially improve it through reverse engineering. Heico claims to have never had a significant issue with any of its replacement parts.

For a manufacturer applying for a PMA, the process includes:

- Applicant must identify the applicable airworthiness standard to the FAA and identify the basis for design approval.

- The two most common paths for design approval are “identicality with a license agreement” and “test and computation.” An applicant seeking a PMA using the identicality path typically enters into a licensing agreement with the OEM and uses the OEM’s drawings in order to make the exact same part. This is typically the case for OEMs who for whatever reason no longer wish to continue to supply a certain part. Using the “test and computation” approach, the applicant must perform analysis and tests to prove that the part is equal or superior to the original OEM part. Only minor changes are allowed from the original OEM part. In this situation, the manufacturer must be careful not to infringe on any patent.

- Identification of the criticality of the part

- This is determined by an analysis of the potential impact of failure for the component as well as the assembly that the component is included in. Every potential means of failure and the potential impact is analyzed. This analysis determines whether the part is deemed as critical (possibly affecting airworthiness of the aircraft), important (possibly affecting the performance of the aircraft or engine) or not critical or important.

- The applicant must also identify if there are any problems or other unresolved issues pertaining to the original OEM part.

- If the part is classified as critical or important, the applicant must present a Project Specification Certification Plan to the FAA providing information on the testing procedures, performance measures and milestones that must be met.

- “Often an applicant will obtain a representative sample of OEM parts and analyze them to establish a benchmark that must be equaled or bettered by the PMA part. Careful dimensional analyses of the OEM part samples establish the part dimensions and tolerances for manufacturing. Various chemical and metallurgical tests are conducted to establish the materials and processes used on the original part. Finally, physical testing is accomplished to determine OEM part’s ultimate strength and response to the operating environment. The PMA part is then designed using the findings from the OEM part sample.”[2]

- This is the part of the process that can become very expensive for manufacturers seeking approval as testing could potentially involve flight time and assessment of the part and how it works in relation to other areas of the aircraft.

- After the part is approved, the manufacturer’s facility and manufacturing process must also be inspected and approved by the FAA.

- The final approval steps include the applicant demonstrating that they have inspection and repair instructions for the part and they must also develop a Continued Operation Safety plan for their part that addresses problem prevention, part monitoring, and problem response.

The length of time to receive a PMA typically takes a few months and possibly longer. Often times PMA manufacturers will work with airlines as well as MRO organizations in deciding for which parts to seek PMA approval. Given the significant investment in money and time required for the PMA approval process, manufacturers typically won’t seek approval unless they feel confident their customers not only want the component but will purchase enough volume to make it worth the investment. From this standpoint, FSG certainly benefits from its relationships with the airlines. From an airline’s perspective, the PMA decision includes several factors including lease arrangements, part complexity and importance, potential cost savings, frequency and volume of replacement, part availability, supplier reliability, track record and financial health, plane resale value and warranty considerations among others. Airlines and MROs may also work with PMA manufacturers during part design and testing.

It is also important to note that the FAA has worked with its counterparts around the world to forge Bilateral Aviation Safety Agreements (BASAs) which ensure the airworthiness of any part originating in any nation that has a BASA with the US. The US currently has BASAs with the EU and most other countries around the world. This is important for PMA manufacturers because for all countries with a BASA with the US, the PMA approval carries over to aircraft operating in those countries. The only exception is with parts deemed critical, for which a PMA may not be sufficient for the foreign authorities. This could be an important consideration when the title of an aircraft transfers to different areas of the world.

- Apple Valuation

- Netflix Valuation

- Microsoft Valuation

- Meta Valuation

- Tesla Valuation

- Amazon Valuation

- Citibank Valuation

- Nvidia Valuation

- AMD Valuation

- Best Buy Valuation

- Alphabet Valuation

- Home Depot Valuation

- JPMorgan Valuation

Resistance to PMA Parts

While price differences vary, the typical PMA component is anywhere from 20% to 50% less expensive than its OEM counterpart. Yet, for a variety of reasons, industry acceptance of PMA parts is still relatively small, although increasing.:

- Airplane lessors have problems with PMA parts due to the potential impact on plane resale value. Around the world, lessors own significant numbers of airplanes, which after leasing, lessors will sell the aircraft or break it down and sell the parts. Given that not all regulatory agencies and all airlines will accept planes with PMA parts, some lessors are reluctant to use them. Even if a lessor sells a plane for parts, they worry that PMA parts may detrimentally impact the plane’s residual value. Currently the lessors, including companies like Aercap, own nearly half the global fleet. Some lessors allow for the use of PMA parts but not all.

- Aircraft owners are sometimes deterred from purchasing PMA parts over concerns that PMA parts may breach the terms of the OEM warranty. This is typically not an issue for new product warranties as they usually cover part replacement. However, the terms of extended warranties may preclude the use of PMA parts. In this situation, the aircraft owner may still benefit by using PMA based on the savings compared to the value of the warranty (if it’s worth much at all), yet this issue can still be a deterrent.

- As expected, OEMs have fought hard against the encroachment of PMA parts on their lucrative businesses. In addition to undertaking advertising campaigns, the OEMs have also threatened not to support their products if PMA subcomponents are used. For example, certain engine OEMs have indicated they would withdraw technical support for their engines if PMA parts were used for engine repair and overhauls. From an airline’s perspective, this would be detrimental as the OEMs have significant engineering knowledge and their support can be valuable if problems arise that are outside the competencies of the airline’s engineers. On the other hand, it is not in the long-term interests of OEMs to frustrate their customers as OEMs benefit from the knowledge gained from having a close working relationship with the airlines and MROs.

- Even though they are FAA approved and have proven as safe as OEM parts, some customers may view PMA parts as imitations and not as good as the original. This perception is similar to individuals who will only get their automobiles serviced and repaired by an official dealership of a particular brand. Part of the issue is perception. No airline purchasing manager wants to be in a position of potentially trying to buy “cheap” parts just to save a few bucks, especially given the potential costs (in terms of safety as well as down time) if there is an issue. This is especially true for critical and life-limited parts.

- Some airlines may use the threat of a PMA part as a bargaining tool to keep a lid on OEM pricing. If faced with the potential loss of a customer, an OEM may be willing to make pricing concessions, especially if margins are already very high, to keep a customer from switching. With margins that are already high in most cases, many OEMs may be well positioned from a financial perspective to fend off competition from PMA suppliers, even if this means a moderation of pricing power. Also, if airlines have a good relationship with a supplier who is responsive and provides excellent service, they may be reluctant to switch suppliers despite the savings, especially for low volume parts.

- Finally, given the collaboration necessary for the development of certain parts, it is easier for airlines and MROs to work with relatively few suppliers with broad products offerings rather than many small suppliers. From the customer’s standpoint, it may not be worth it if it must coordinate with a host of additional suppliers and/or distributors.

Despite the difficulties and barriers to selling PMA parts, Heico has been very successful. In the PMA parts business, scale is very important, especially considering the costs associated with gaining FAA approval. Heico has benefitted from a virtuous cycle as it partners with more airlines and MROs:

- More airline and MRO partners lead to greater collaboration and increasing numbers of parts produced for more of the global fleet.

- Greater product offerings on an increasing number of platforms lead to more airline customers and increased penetration with existing customers resulting in a virtuous cycle.

- Greater numbers of the same parts sold to more customers significantly lowers development and approval costs per unit.

- This is an important point highlighting an advantage Heico has over other companies which manufacture PMA parts: Heico has a scale advantage when it comes to development and approval costs as well as distribution and customer servicing capabilities.

- As the largest producer of PMA parts with a decades-long history of producing quality parts, Heico has a positive reputation as well as an understanding and agreements with the FAA which expedites the part approval process.

- Greater production volume provides leverage to fixed costs which has led to small increases in margins over time but also greater savings passed to customers (i.e scale economies shared), further increasing customer goodwill.

- Ultimately, the more PMA products Heico sells to its customers, the profitability of its customers increases – not many businesses can claim this.

Financial Performance

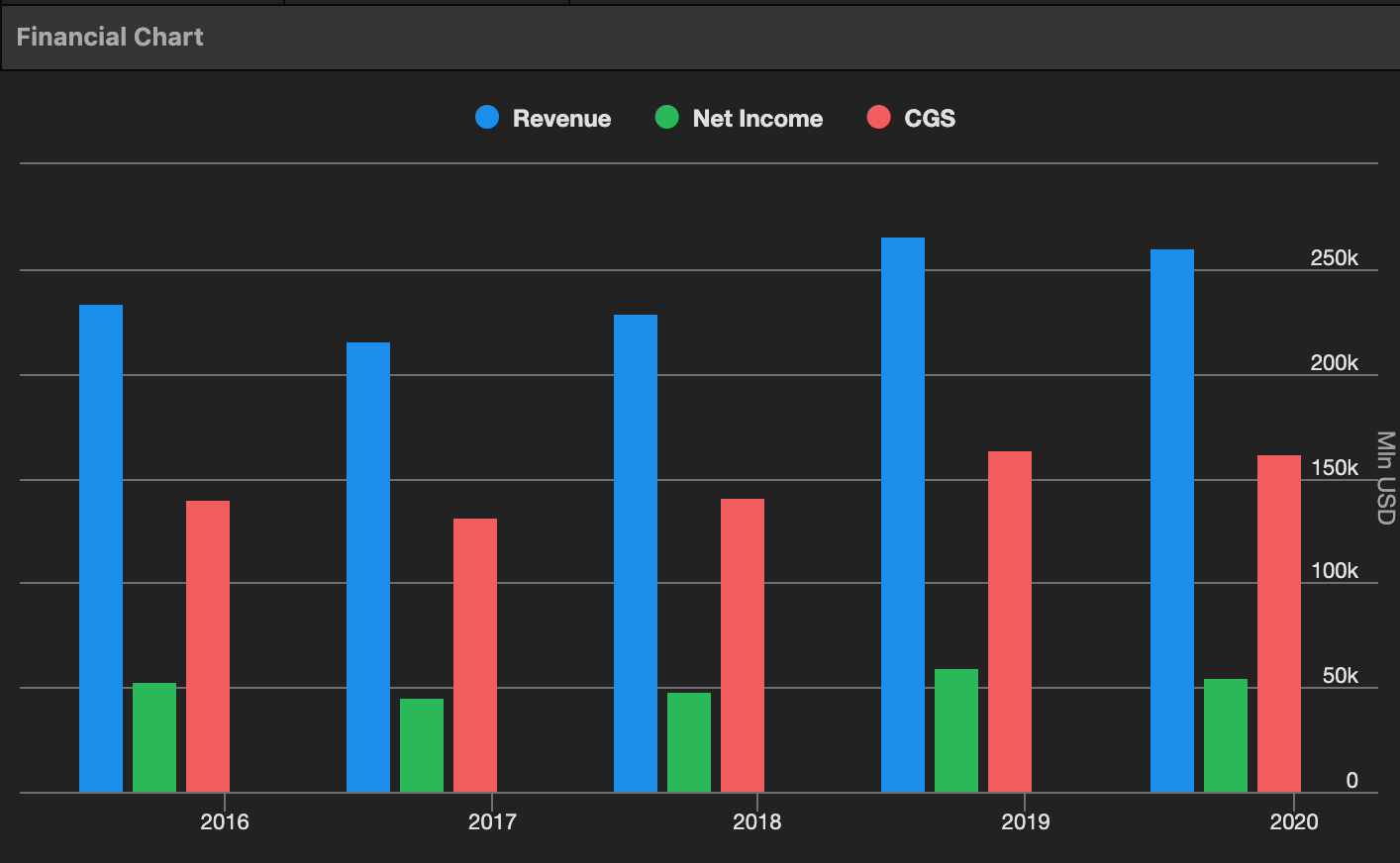

Over the past decade through FY 2022, sales have increased at a compound annual rate of 9% despite the pandemic hitting FSG very hard the past couple of years. This growth has been roughly half organic and half from acquisitions. Both FSG and ETG have contributed, growing at compound annual rates of 8.2% and 11.4%, respectively, over ten years. The pandemic led to flat FSG revenue from FY 2019 to FY 2022, while ETG compounded at 5.2% over that period. For the decade prior to the pandemic, overall revenue had compounded at 13% annually. Despite the fact that global air travel hasn’t yet reached pre-pandemic levels, 2022 revenue for FSG slightly surpassed the previous peak of $2.056 billion from 2019, with growth in PMA specifically, increasing 2.4% above 2019 levels.

The average and median annual organic revenue growth over the past decade for FSG and ETG have been 4.8% and 6.5%, and 3.4% and 3.0%, respectively. Prior to the pandemic, FSG’s organic growth averaged 7.5% per year. The largest factors underpinning organic growth are the increased unit volume of aftermarket replacement parts for FSG and growth in niche markets in ETG. Typically, Heico takes very little pricing. The aftermarket replacement parts business is growing due to taking increased market share in an overall market characterized by long-term secular growth. Revenue Passenger Miles (RPMs), the primary metric for assessing growth in air travel, are defined as paying passengers multiplied by miles traveled. Based on data from the US Department of Transportation, RPMs for US-based airports have grown by about 2.5% annually for the past 15 years prior to 2020. Global RPMs have increased annually by around 5% over recent decades. According to Boeing’s current market outlook, global commercial air travel is projected to grow by approximately 6% annually for the next twenty years, driven by growth in Asia, Africa, and the Middle East.[3] Assuming historical global RPM growth of 5% and minimal price increases, FSG’s organic growth indicates growing market share.

Over the past decade, gross margins have been extremely steady, averaging 37.8% and ranging from 35.2% to 39.1%. During this time, there has been some leverage to operating expenses as they have decreased as a percent of sales from 18.6% in 2013 to 16.6% in 2022. Over the past decade, the EBITDA margin has increased from the low 20% range to 26.6% in 2022.

As mentioned previously, the company has made almost 100 deals since the Mendelson family took control of the company. Over the past five years, Heico has acquired, on average, 1.5% of its market cap annually. However, over the ten years prior to that, the company acquired, on average, approximately 6.6% of its market capitalization annually. This bounces around a lot year to year; however, it’s noteworthy that as Heico’s market cap has ballooned in recent years, the acquisition spend relative to the market cap has been quite low relative to prior years. For example, 2022 was the second largest year in terms of acquisition spend in history, yet the total spend only equated to 2.2% of the market cap.

Acquisitions have been critical to Heico’s success over the long term and remain critical moving forward. The company is a disciplined acquirer. The company views acquisitions more as a way to compound cash flow rather than buying to fulfill some strategic vision. Larry Mendelson made the following comments at a sellside conference two years ago: “The business of HEICO, I've often said, is not commercial aviation nor is it ETG. It's a vehicle for generating strong cash flow and making profit. And how do you do that? You acquire or develop businesses that have unique characteristics and unique markets, generally speaking, protected markets, niche markets, where it's difficult for other people to compete because of either technology, not really patents, but sometimes that. But it's really the ability and the talent of the individual and the niche in which they're operating. So all of the businesses that we acquire have those characteristics. And they're unique businesses. Lots of other people wouldn't really understand them, but they're run by entrepreneurial people in a decentralized manner. And they add to HEICO's snowball of cash, but they have to have some special leg up that makes them very unique and very difficult to compete with, thereby assuring good margins and strong cash flow. And that's really what we look for. And they can be in diverse businesses.

When looking for deals, Heico is opportunistic, looking for companies with certain characteristics such as highly technical (yet relatively slow-moving technology), critical components which are typically integrated into a larger system or assembly for products not prone to rapid change (i.e. missile defense systems, locator beacons, etc.). These products are usually low volume and relatively low-cost compared to the overall value of the final product, but highly important, which helps to both insulate from competition but also produce strong margins. From a financial standpoint, they want to see growth with healthy operating margins (20%+) and high cash conversion. Because of the decentralized culture and the fact that Heico leaves a minority ownership interest with the selling entrepreneur to align incentives, they also place a lot of emphasis on the reputation, integrity, and honesty of the seller entrepreneur. Once acquired, the businesses are usually run by the same people who sold them (maybe 20% of deals have been folded into an existing Heico company). From the 2007 annual report: “Overall, our entrepreneurial acquisitions have worked very well. We distinguish ourselves from larger entities by emphasizing to sellers/founders that we recognize the value which they bring to the business and generally want to retain their separate operations or identities. People who have sold us their companies recognize that our strategy is not to merely dismember the business which they have built. Simultaneously, though, we have made, and will continue to make, acquisitions of less entrepreneurial businesses where there are consolidation opportunities.”

Many of Heico’s acquisitions have become part of ETG and are why ETG has grown faster than FSG over time. Acquisitions are usually paid in cash, not stock, and funded using a revolving credit facility which is quickly repaid to keep leverage low. While Heico doesn’t actively talk about synergies, there are certain ways in which being part of Heico benefits acquired companies. First, it provides quick and easy access to capital to fund growth without having to take on debt or raise additional capital. Along those same lines, the financial strength of Heico can help enable an acquired company to gain contracts with large customers who otherwise may not work with such small, undercapitalized suppliers. Also, Heico has been successful at helping acquisitions grow by introducing them to new customers while having instant credibility by being part of Heico.

One of the reasons the acquisitions program has generated so much equity value is that Heico is disciplined in how much it is willing to pay. Larry Mendelson often comments how Heico won’t pay excessive multiples for acquisitions. From the Q4, 2021 call: “And you know the standards we look at are the cash payback in 7 to 10 years, and we don’t want to pay 14x EBITDA with pie in the sky in the future and so forth. So that strategy has served us very well, and we’re going to continue that strategy.” I respect the pricing discipline the company has shown, especially in recent years when the stock has traded at an EV/EBITDA multiple probably close to 3x compared to what it pays for acquisitions.

For the past decade returns on invested capital (ROIC) have averaged 16.3%, which is significantly in excess of Heico’s cost of capital. The company’s investments in both additional capital assets as well as acquisitions have produced attractive incremental returns. For example, over the past five and ten years, cumulatively, every dollar invested in capital expenditures and acquisitions has led to incremental returns on that capital of 19.6% and 15.3%, respectively. Heico’s acquisition strategy has been a key factor that has caused the stock price to compound over time. The company generally doesn’t do mega-deals, but rather it focuses on smaller deals to ensure breadth of products lines across multiple platforms and industries. The company has also focused on buying privately-owned, founder-run businesses:

Valuation

Based on a current stock price of $139 for the A shares, Heico’s current market cap is $19.3 billion and its enterprise value (EV) is $19.9 billion. The share count includes the shares which will be issued for the Wencor acquisition. The common shares currently trade for $171 per share; however, I’m basing the value off the price of the A shares. As previously mentioned, the two share classes have identical economic rights.

Admittedly, the multiples in the table above look quite expensive even after the stock price has essentially gone sideways for over two years. The price today is the same as the price in May of 2021. So why am I recommending the stock today given the valuation?

Why Buy the Stock

Given recent acquisitions, ongoing organic growth, plus a continuing recovery in global air travel, while the stock price today looks expensive, if investors can look out a couple of years, I think the price is much more reasonable given the quality of the company. In January of 2023, Heico spent approximately 467 million Euro to acquire Exxelia, which is a designer and manufacturer of high reliability electronic components and rotary joint assemblies for mostly aerospace and defense applications. Exxelia’s revenue in 2022 was 190 million Euro with operating margins slightly below the ETG average. In May of this year, Heico announced the $2.05 billion acquisition of Wencor, its largest competitor in the PMA space with over 6,000 PMAs. Heico is financing the deal with $1.9 billion in debt and $150 million in equity. Wencor’s revenue and EBITDA for calendar 2023 are anticipated to total $724 million and $153 million, respectively. This deal alone will increase Heico’s EBITDA by 21% while costing it just under 11% of its EV.

Like FSG, Wencor has a PMA business as well as distribution and MRO assets for the commercial and military aftermarkets. Heico believes this transaction will be very complementary as there is little to no overlap of the PMAs produced by each company. Obviously, to take advantage of the OEM pricing umbrella, PMA companies compete with the OEMs, not each other, so PMAs are rarely duplicated. On the most recent conference call, the company pointed out that Heico’s component repair stations already purchase most of Wencor’s PMA components because Heico doesn’t make those products. The company also pointed out that there is not a lot of overlap in both the maintenance and repair businesses and the distribution businesses. In other words, Heico will now offer a much broader portfolio of products and services to better serve the needs of its customers. There will be significant cross selling opportunities:

The consensus revenue expectation for FY 2023 is $2.74 billion which includes approximately 20% organic growth from FSG, a LSD organic revenue decline from ETG, a partial year’s revenue from Exxelia, and revenue from 2022 acquisitions. Assuming LDD organic revenue for FSG and LSD organic revenue growth from ETG (assuming military spending picks up), over $800 million in revenue from Wencor (assuming it is acquired on Nov 1, the start of Heico’s fiscal year and LDD organic growth from CY 2023 levels), and the annualization of a full year of Exxelia’s revenue, total revenue comes to over $3.8 billion in FY 2024. After the acquisition of Wencor, FSG’s organic revenue growth will be supported by obvious cross selling opportunities as well as continued growth in global RPMs as they catch up to pre-pandemic levels. For FY 2025, once Wencor synergies start to flow and global air travel continues to grow, revenue and EBITDA will likely approach $4.2 billion and $1.1 billion, respectively. As Heico quickly repays the Wencor debt, free cash flow will grow rapidly, likely, depending on the speed of debt paydown, totaling near $700 million in FY 2025 and approaching $800 million within the next year or two. This doesn’t contemplate further M&A as the company will likely devote nearly all free cash flow to paying down the Wencor debt, but depending on how quickly the debt is paid down, net leverage could be below 1x by the end of FY 2025, after which the M&A machine will resume. Based on these assumptions, I think the stock can compound at a HSD rate over the next five years, even assuming some multiple contraction. There is upside to the potential return if M&A picks up sooner than anticipated and/or the Wencor deal provides greater benefits than anticipated. While this certainly isn’t a “cheap” valuation, I think this is the best opportunity to buy the stock since the pandemic selloff in early 2020.

Negatives/Risks

- The primary negative surrounding Heico is that the stock price is not cheap. As previously mentioned, the stock price hasn’t done much for the past 2.5 years as the valuation in 2021 became extreme. Some of that extreme has been worked off but the valuation multiples are still somewhat elevated. While I don’t think the expectations I’ve spelled out are excessively optimistic, if the Wencor acquisition underperforms or multiples decline for any reason, near term returns could be poor. Outside of the pandemic, the stock hasn’t been cheap since the first quarter of 2016 when you could buy the A shares for a 6% free cash flow yield. While I don’t think the stock will trade back to a 6% free cash flow yield, it could certainly trade at lower multiples compared to current levels. However I think this is a near-term price risk, not something that could lead to a permanent impairment given Heico’s very low leverage levels and organic growth tailwinds.

- As longtime Chairman and CEO, Laurans Mendelson, is 84, he will likely not remain in these positions for too much longer. His sons, Eric, who is the Co-President and President and CEO of FSG and Victor, who is the Co-President and President and CEO of ETG, have long tenures at the company and are without question very capable. However, it is unclear who will lead the company after the current CEOs departure or if Eric and Victor may share responsibilities as their current titles of Co-President suggest. I think it makes a lot of sense for FSG and ETG to remain together, but who knows what the future holds?

- While the A shares are cheaper than the Common, they also have 1/10 of the voting rights. Including insiders and one large, friendly individual shareholder (who initially invested with the Mendelsons when they took over the company), over a quarter of Heico’s votes are held or influenced by the Mendelsons. This voting block is effectively large enough to control the company. Heico is basically a publicly traded family business. Should the Mendelsons begin making questionable decisions, there is little owners of the A shares could do to influence the company. On the other hand, the A shares trade at a discount to the common to reflect the voting difference. Also, over long periods of time, the returns to the two share classes have been close. This is likely because the A shares have always been cheaper than the common. Also, given how well the Mendelsons have managed the company over the past 30 years, I question how much more valuable the extra votes per share are worth. If a potential investor questioned the capabilities of the Mendelson family, the answer would be to choose to not buy the stock in the first place, not buy the Common as that would likely be of no use given the control the family already has.

- I think the biggest risk longer-term is that the impact of the very successful acquisition program wanes as Heico’s ability to acquire can’t keep up with its market cap. For example, the chart earlier in the writeup (reflecting annual acquisition spend and acquisition spend as a percentage of the market cap) shows that prior to Heico’s valuation moving higher in 2018, the company was routinely able to acquire a HSD percentage of its market cap in most years. However, now that the market has somewhat recognized the high quality of the company, its ability to recycle significant percentages of its market cap into acquisitions isn’t what it once was. For example, for the five years from 2018 through 2022, Heico was only able to acquire 1.5% of its market cap on average, per year. For the seven years prior to 2018, it acquired, on average, 7.3% of its market cap per year which helped to rapidly compound the value of the company. On the one hand, making acquisitions at 12x EBITDA and then having the market immediately revalue that EBITDA to 28x certainly enhances the value of the company. However, the market can be fickle, multiples can change, and I’d prefer to compound value without having to rely on multiple arbitrage. Conversely, with Exxelia and Wencor, its two largest acquisitions, Heico has been able to invest significant amounts of capital so maybe this worry is unfounded.

Conclusion

Heico is a very good business run by proven capital allocators operating in a growing industry. As the largest competitor in the PMA component market, especially after the Wencor acquisition, the company has significant scale and will continue to gain market share over time as PMA parts gain share in the aftermarket. Additionally, the company will continue to carry out its highly effective acquisition program which will likely continue to create value for shareholders, regardless of the multiple at which the stock trades. If investors can look a couple of years down the road, especially once Wencor and FSG have the opportunity to collaborate, the market is offering the stock of a wonderful company at a fair price. However, most importantly, I think Heico’s management team, maybe more than any other I’ve ever encountered, is committed to treating shareholder capital as if it is its own. The Mendelsons not only say, but have done the right things for many years. As mentioned previously, Heico is essentially a family-run business with minority public shareholders along for the ride. It’s a ride which I plan to stay on for a very long time. From the Q4 2021 call: